Transportation plays the most important role in the economy of India as it connects all the businesses concerned with goods. Any changes or problems in transportation sections always affects the the entire business channel. Goods transportation is done by road, by rail, by vessels and by air. Here we are going to discuss about changes in GST in Goods Transportation by road. Recently there was 47th GST council meeting, in this meeting certain changes in GST on transportation of goods by road were recommended and accordingly now the notification has been issued. So we are going to discuss here about these changes

GST notification on goods transport agency

What is the gst rate on transportation of goods is always important to understand. There is notification 11/2017 Central Tax (Rate) for gst rates on various services. Item no iii of sr no 9 of this notification is for transportation of goods by goods transport agency. Now the item no iii of sr no 9 of notification 11/2017 Central Tax (Rate) has been amended by Notification 03/2022 Tax (Rate) dated 13.07.2022. Effective from 18.07.2022

What is goods transport agency in GST?

Before we learn about recent changes in goods transport agency in gst, first we lets understand meaning of goods transport agency.

In para 4 relating to Explanation, new clauses inserted in Notification 11/2017 Central Tax (Rate) by Notification 03/2022 Tax (Rate) dated 13.07.2022 defining the meaning of goods transport agency as under

Any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called.”;

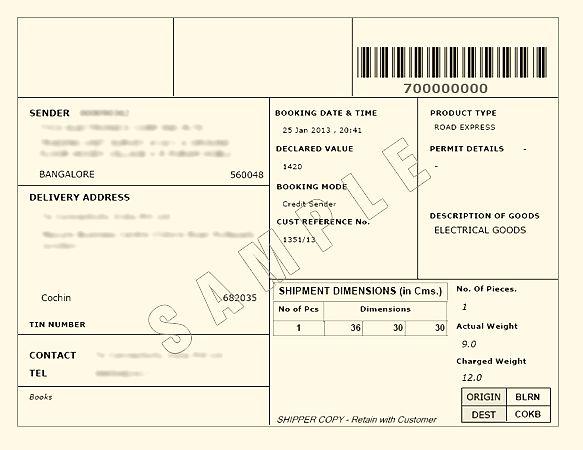

What is Consignment Note under GST?

A consignment note is a document issued by a goods transportation agency against the receipt of goods for the purpose of transporting the goods by road in a goods carriage. If a consignment note is not issued by the transporter, the service provider will not come within the ambit of the goods transport agency.

If a consignment note is issued, it means that the lien on the goods has been transferred to the transporter. Now the transporter is responsible for the goods till it’s safe delivery to the consignee.

A consignment note is serially numbered and contains –

- Name of consignor

- Name of consignee

- Registration number of the goods carriage in which the goods are transported

- Details of the goods

- Place of origin

- Place of destination.

- Person liable to pay GST – consignor, consignee, or the GTA.

Format of Consignment Note for GTA

One more new option to pay GST in Goods Transport Agency w.e.f 18.07.2022

- Now with effect from 18.07.2022 Goods transport agency (GTA) is being given option to pay GST at 5% or 12% under forward charge

- option to be exercised at the beginning of Financial Year. RCM option to continue.

Let’s understand this amendment in simple way

- Position before the amendment

| Option | Position |

| Option of reverse charge | RCM will be applicable 5% GST will be paid by service recipient NO ITC will be taken by GTA |

| Option of forward charge | RCM will not be applicable GTA will charge 12% GST in its invoice No restriction in taking ITC by GTA Liable to pay GST @ 12% on all the services of GTA supplied by it |

Note: There was no any mechanism for informing the option exercised.

- Position after the amendment

| Option | Position |

| If GTA does not exercise option | RCM will be applicable 5% GST will be paid by service recipient NO ITC will be taken by GTA |

| If GTA exercise option to pay GST @ 5% GST | RCM will not be applicable GTA will charge 5% GST in its invoice NO ITC will be taken by GTA |

| If GTA exercise option to pay GST @12 GST | RCM will not be applicable GTA will charge 12% GST in its invoice No restriction in taking ITC by GTA |

Under this new amendment GTA will have to take following care

- The option by GTA to itself pay GST on the services supplied by it during a Financial Year shall be exercised by making a declaration in Annexure V on or before the 15th March of the preceding Financial Year:

- The option for the Financial Year 2022-2023 shall be exercised on or before the 16th August, 2022:

- Invoice with GST 5% or 12% may be issued during the period from the 18th July,2022 to 16th August, 2022 before exercising the option for the financial year 2022-2023 but in such a case the supplier shall exercise the option to pay GST on its supplies on or before the 16th August,2022.”;

Format of form for exercising the option by a Goods Transport Agency (GTA)

In Annexure V of Notification 11/2017 Central Tax, a form for exercising the option by GST has been provided which is as under

FORM

Form for exercising the option by a Goods Transport Agency (GTA) for payment of GST on the GTA services supplied by him under forward charge before the commencement of any financial year to be submitted before the jurisdictional GST Authority.

Reference No.-

Date: –

1. I/We______________ (name of Person), authorised representative of M/s……………………. have taken registration/have applied for registration and do hereby undertake to pay GST on the GTA services in relation to transportation of goods supplied by us during the financial year……………under forward charge in accordance with section 9(1) of the CGST Act, 2017 and to comply with all the provisions of the CGST Act, 2017 as they apply to a person liable for paying the tax in relation to supply of any goods or services or both;

2. I understand that this option once exercised shall not be allowed to be changed within a period of one year from the date of exercising the option and will remain valid till the end of the financial year for which it is exercised.

Legal Name: –

GSTIN: –

PAN No.

Signature of Authorised representative:

Name of Authorised Signatory:

Full Address of GTA:

(Dated acknowledgment of jurisdictional GST Authority)

Note: The last date for exercising the above option for any financial year is the 15th March of the preceding financial year. The option for the financial year 2022-2023 can be exercised by 16th August, 2022.]

FAQS for GST on GTA

What are the services provided by a GTA?

The service includes not only the actual transportation of goods, but other intermediate/ancillary service provided such as-

Loading/unloading

Packing/ unpacking

Trans-shipment

Temporary warehousing etc.

If these services are included and not provided as independent activities, then they are also covered under GTA.

Who will pay under Reverse Charge?

If GTA does not exercise option RCM will be applicable,5% GST will be paid by service recipient. NO ITC will be taken by GTA.

Is a GTA liable to register?

There was a lot of confusion about whether a GTA has to register under GST.

As per Notification No. 5/2017- Central Tax dated 19/06/2017, a person who is engaged in making only supplies of taxable goods/services on which RCM applies is exempted from obtaining registration under GST.

Thus, a GTA does not have to register under GST if he is exclusively transporting goods where the total tax is required to be paid by the recipient under reverse charge basis (even if the turnover exceeds the threshold limit).

Can GTA pay GST on forward charge?

Yes, before 18.07.2022, GTA was having option to pay GST @12% under forward charge. Now w.e.f 18.07.2022, GTA is having two options to pay GST on forward charge. One is pay GST @5% on forward charge without claiming any ITC and another option is pay GST @12% on forward charge with claiming ITC

Read more articles

GST Rates on works contract services w.e.f 18.07.2022

Key Decisions of 47th GST Council Meeting

GST e-invoice applicable to entities having turnover more than Rs 20 cr (from 01.04.202)

CBIC issues Guidelines for Recovery Proceedings under CGST Act, 2017